Value sales growth for the carbonates category is slowing in the same way as other impulse categories, as price inflation slows and volume recovery fails to offset the price growth slow down.

Value sales growth for market was up 6.6% in the year to end of November 2023, versus the year to November 2022, but growth in the latest four weeks versus the previous year has slowed to up just 1.1% versus last year, someway behind the latest four-week growth across impulse, which is up 7.3% vs last year in the latest four weeks.

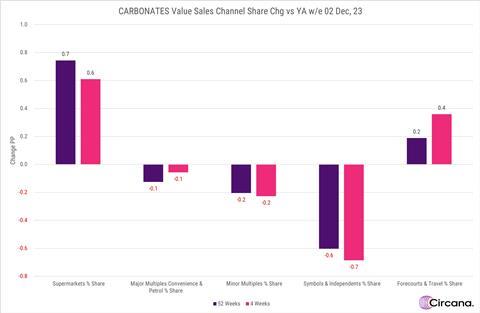

Carbonate growth slowdown is more evident in symbols and independents which saw a decline of 2% on last year’s value sales in the last four weeks. As a result, the symbols and independent channel lost value share of carbonates in the last four weeks, down 0.7PP on last year and down 0.6PP in the year to November 2023 versus the previous year, with supermarkets gaining value share as volume moves from convenience to supermarkets reflecting the trend seen across other categories.

What’s next in soft drinks?

Traditionally the cold weather leads to a dip in soft drinks sales as shoppers look to stay warm, however recent research by Suntory Beverage & Food UK & Ireland found that the sales throughout the year are more consistent than they’ve ever been with more people buying soft drinks outside of summer. Functional and healthier drinks have played a big part in this, and that trend shows no sign of abating in 2024 meaning retailers need to be ready for a growth in demand in this part of the category. While we’re out of the Christmas party season, the tightening of belts means more big nights in at home which could lead to take-home size formats as consumers seek more affordable treats in January.

No comments yet